The Engine of Global Capital: Fed Policy, Bonds, and Order-Flow Drift

How the Fed reaction function, bond yields, and institutional order splitting turn macro data into persistent order-flow drift.

The Fed reaction function: two mandates, one market joystick

The Federal Reserve is not trying to make EURUSD, equities, gold, or bonds move in a straight line. It is trying to balance two mandates: price stability and maximum employment. Price stability is usually framed around 2% inflation, with PCE as the Fed's preferred measure and CPI as the market-moving release most traders watch first. Maximum employment is tracked through NFP, the unemployment rate, wages, participation, jobless claims, JOLTS, and related labour data.

When inflation is the dominant problem, the Fed tightens policy. Higher rates make credit more expensive, slow borrowing, cool demand, and increase the reward for holding dollars and Treasury assets. When unemployment becomes the dominant problem, the Fed cuts rates. Cheaper credit supports demand, but it also reduces the yield advantage of holding dollars.

This is the first engine behind global capital flow: markets are constantly repricing which mandate is currently forcing the Fed's hand.

- Top-of-cycle problem: inflation. Policy response: restrictive rates.

- Bottom-of-cycle problem: unemployment. Policy response: easier rates.

- Trading edge starts when markets begin pricing the next policy path before the Fed actually moves.

Why the bond market leads the story

The bond market is the institutional control panel. A bond yield is not just a number; it is the price of time, inflation risk, credit risk, and policy expectation. When markets expect the Fed to stay restrictive, front-end yields stay supported and the dollar tends to retain a yield advantage. When markets expect cuts, yields usually fall and the dollar can lose support.

A yield-curve inversion matters because it says the market believes current policy is tight enough to slow the economy and eventually force cuts. That does not mean recession begins tomorrow. It means the bond market is already pricing a future policy response before the labour market or GDP fully confirms it.

This is why FX is often the shadow of the bond market. EURUSD does not only trade US data or Eurozone data in isolation. It trades the difference between the expected Fed path and the expected ECB path.

- Fed expected more hawkish than ECB: USD tends to strengthen, EURUSD pressured.

- Fed expected to ease faster than ECB: USD tends to weaken, EURUSD supported.

- Both central banks turning dovish together: EURUSD often becomes rotational instead of directional.

Markets trade expectations, not announcements

A common retail mistake is waiting for the Fed to actually cut or hike. Institutions rarely wait that long. They model the probability of future policy from CPI, PCE, NFP, unemployment, wages, ADP, JOLTS, jobless claims, ISM, and financial conditions. When those probabilities shift, portfolios adjust before the central bank meeting.

If the market starts expecting cuts, Treasury yields can fall months before the first cut. Gold can catch a bid because the opportunity cost of holding a non-yielding asset falls. The dollar can weaken because the risk-free yield advantage is no longer as attractive. If the market starts expecting hikes, yields rise, gold often struggles, the dollar can strengthen, and equities may face valuation pressure.

The important word is expecting. The market is an anticipation engine, not a newspaper reader.

- Soft labour + cooling inflation: markets price easier policy.

- Hot inflation + stable employment: markets price restrictive policy.

- Hot inflation + rising unemployment: markets become conflicted because both mandates are under stress.

How macro becomes order-flow autocorrelation

Once a large bank, macro fund, or real-money manager changes exposure, the order cannot be executed all at once. Size has to be split. A parent order becomes many child orders, executed over time and across venues. That creates persistent signed flow: buying tends to be followed by more buying, or selling tends to be followed by more selling.

That persistence is order-flow autocorrelation. It does not mean every candle moves in a straight line. It means the next burst of aggressive flow is no longer random because a larger participant may still be working inventory. Other algorithms detect the pressure, join the move, and trapped countertrend traders become forced liquidity when their stops trigger.

A macro thesis therefore becomes visible intraday through cumulative delta slope, session pressure, value migration, and trapped-liquidity feedback.

- Persistent delta in the same direction suggests a parent-order footprint.

- POC and value migration show whether the market is accepting the new price area.

- Retail trapped against the move can become continuation fuel.

The practical Trading Analytica read

The system should not claim to see the full global interbank book. Spot FX is fragmented. What the system can do is read a stack of proxies: cumulative delta, session pressure, bid/ask behaviour, prior value, POC migration, retail positioning shelves, and nearby stop pools.

One metric is noise. Agreement across several independent layers is information. A strong macro catalyst with persistent delta and higher value acceptance is a drift environment. A mixed macro tape with price snapping back to POC is a rotational environment. That distinction decides whether the trader should follow pullbacks or fade extremes.

The goal is not to predict every candle. The goal is to know when random-looking price action has become persistent flow.

- Macro gives the reason.

- Bonds and yield spreads show where capital is being rewarded.

- Auction value gives the location.

- Liquidity and delta show whether the move is executable.

Use the platform as a decision process.

The goal is not to copy one level. The goal is to learn how auction value, retail behavior, liquidity pressure, delta, and risk rules combine into a trade idea.

Related insights

All insights

Trading the Rotational Fight: EURUSD After Weak NFP and Softer Eurozone CPI

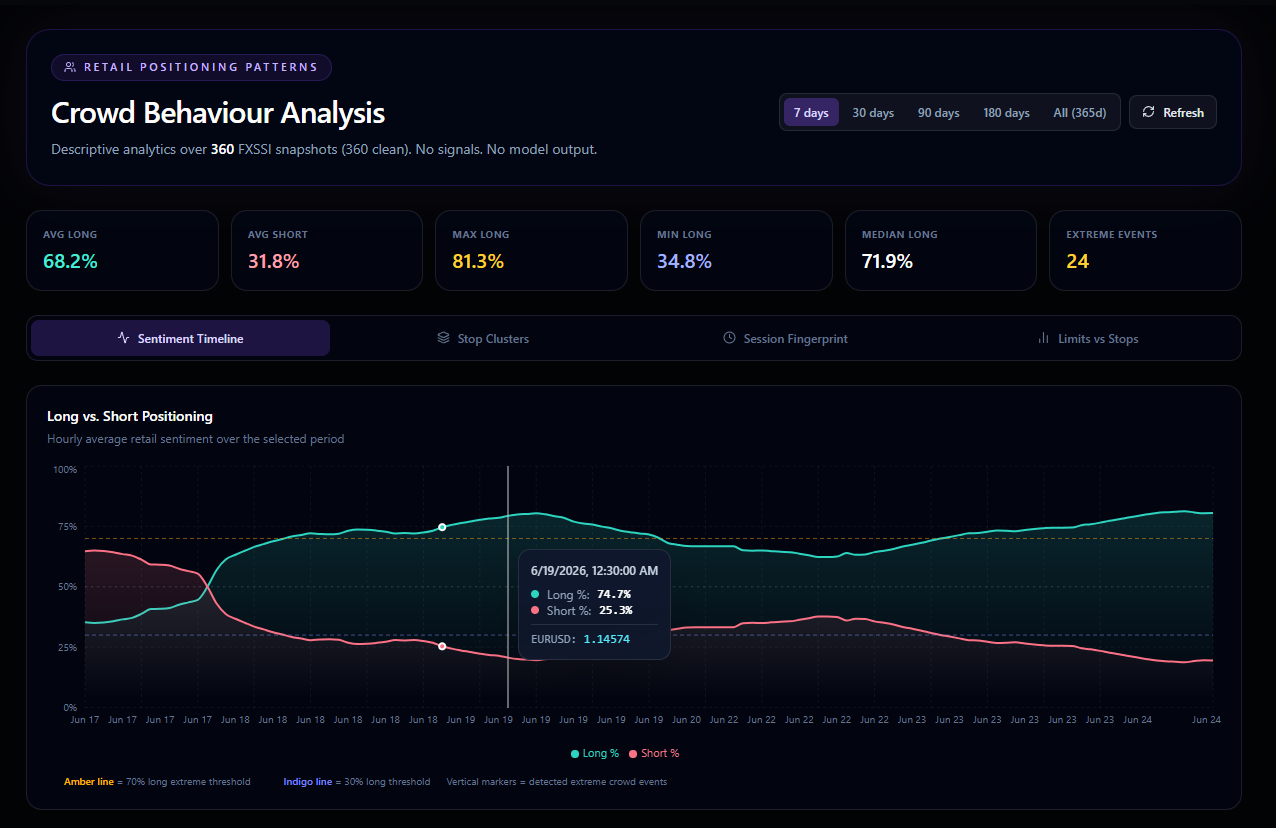

Retail Positioning Patterns: How We Read Crowd Behaviour Without Turning It Into A Blind Signal