How Banks Trade Forex: Order Flow, Algorithmic AI Models, and Dynamic Delta Hedging

An inside look at how institutional FX desks use client order flow, Reinforcement Learning models, and dynamic delta-gamma hedging to operate market-neutral systems.

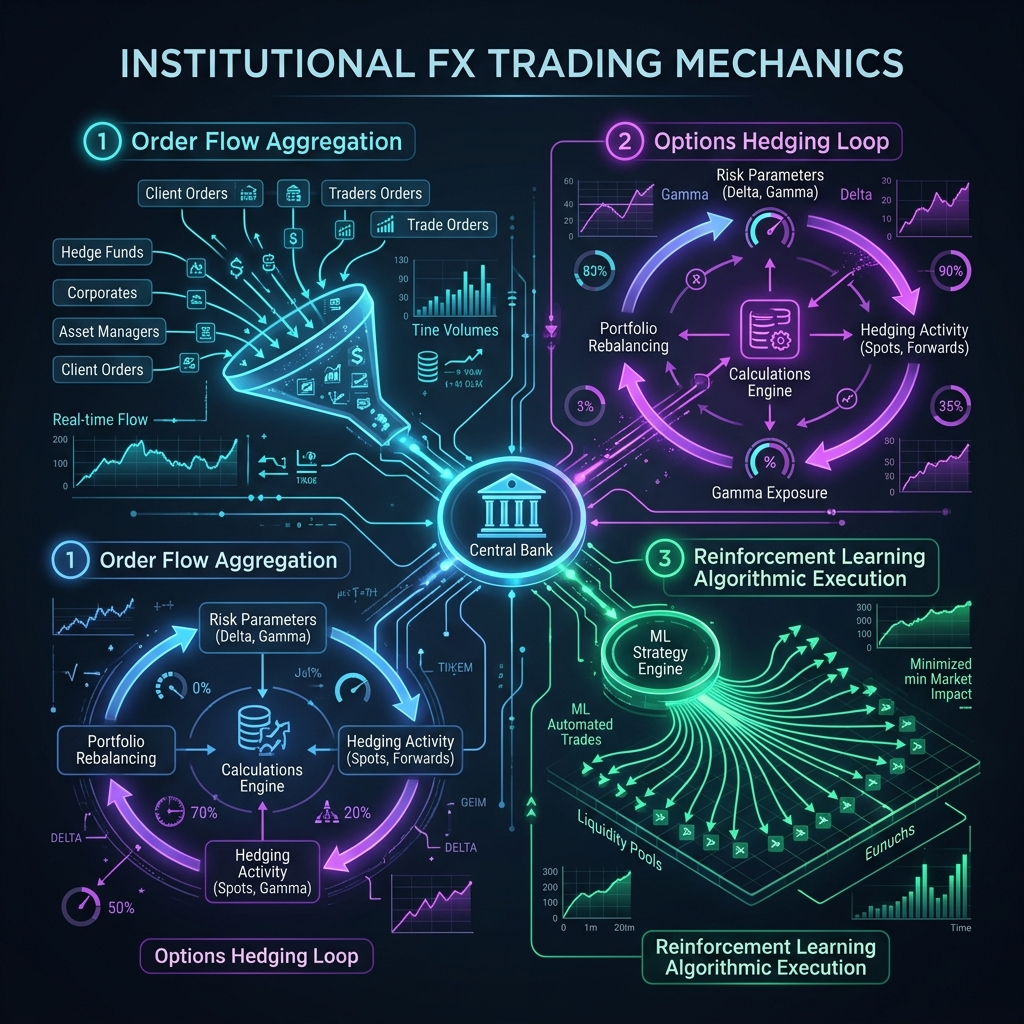

The Microstructure of Interbank FX: It is all about Order Flow

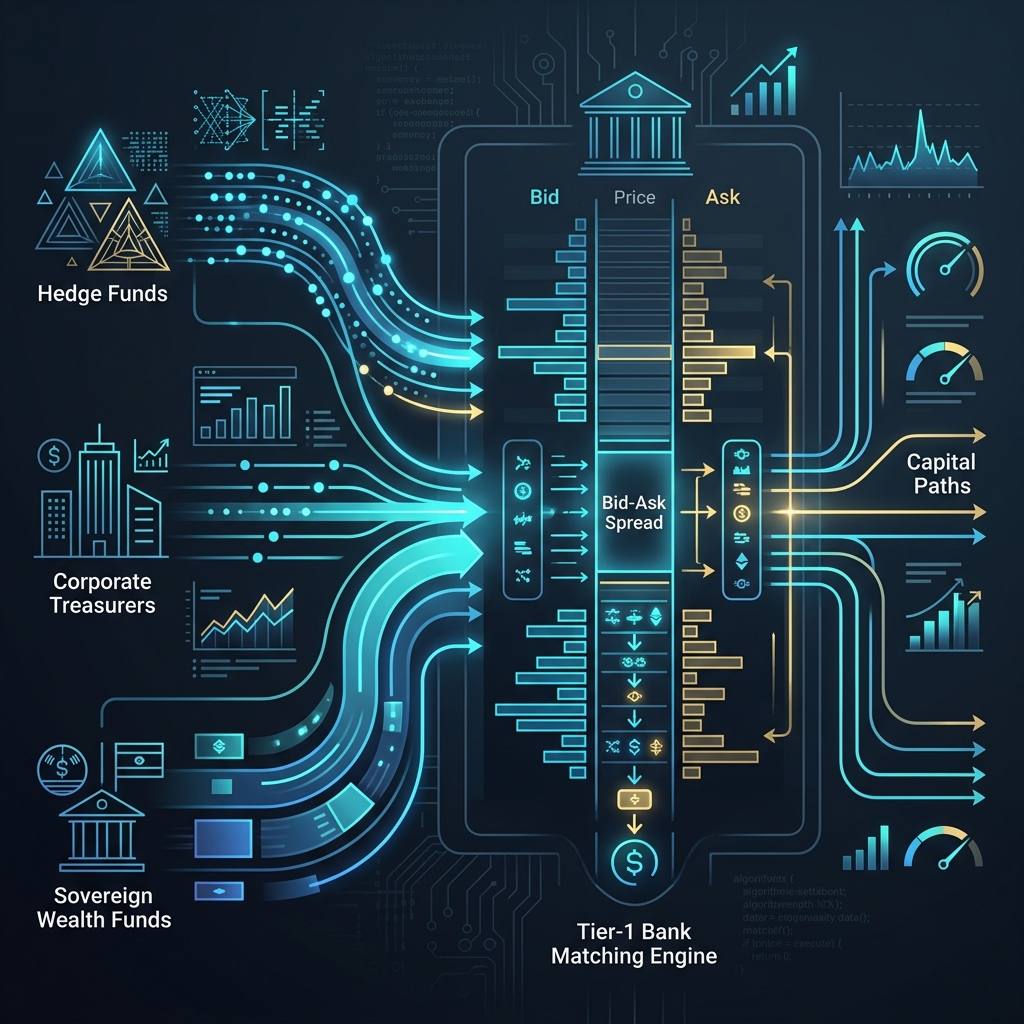

In the foreign exchange market, tier-1 investment banks (primary dealers) operate as market makers. They do not place directional bets or gamble on where EURUSD will trade next week. Instead, their business model revolves around capturing the bid-ask spread and maintaining a market-neutral book.

The ultimate driver of exchange rate movements is not public economic news itself, but how that news is processed through client order flow. According to the foundational paper 'Order Flow and Exchange Rate Dynamics' (Evans & Lyons, 2002), order flow is the vehicle through which private information about fundamentals is incorporated into the exchange rate. Because banks sit at the center of this capital flow, they observe transaction queues from hedge funds, corporate treasurers, and sovereign wealth funds. This aggregate volume log provides them with a superior view of institutional commitment before it appears on retail price charts.

How Banks Deploy Machine Learning on Spot Desks

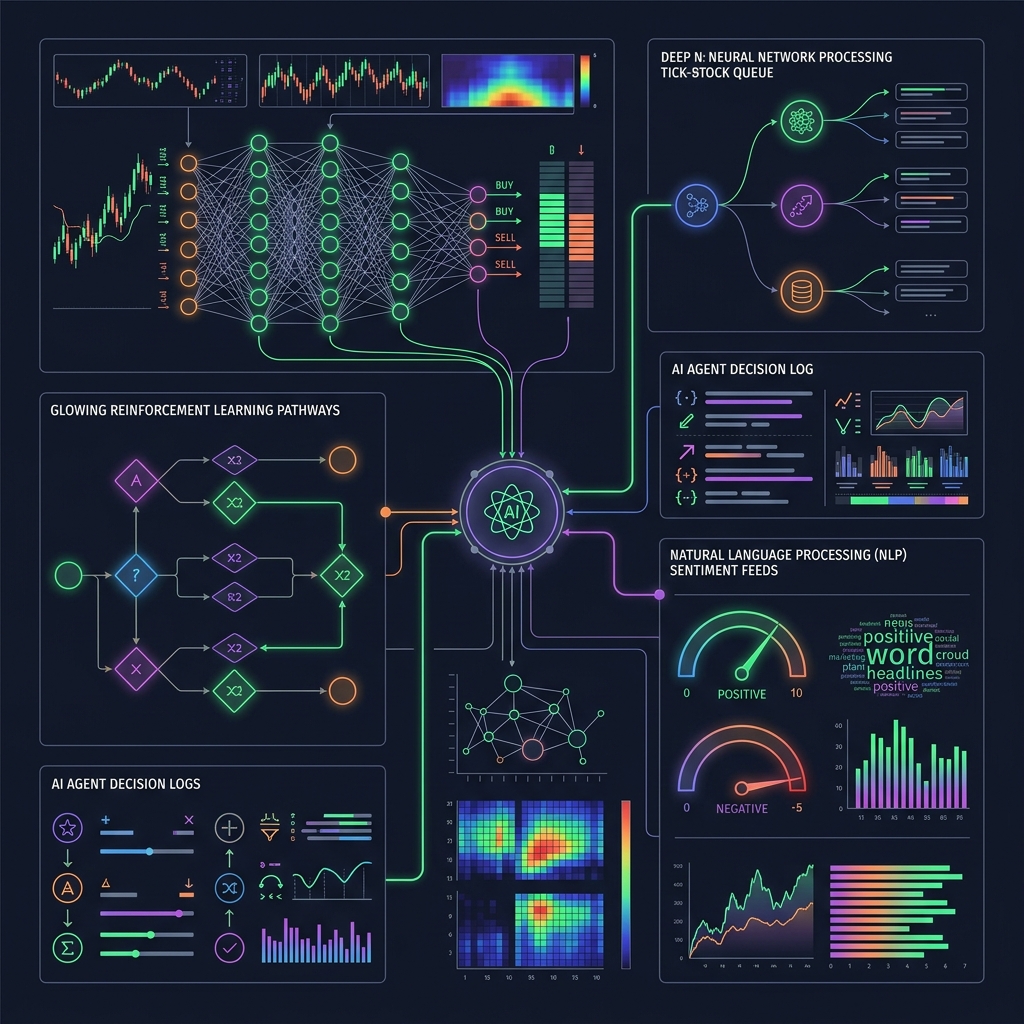

Banks deploy AI and machine learning algorithms not to guess the future, but to solve execution and inventory problems. Rather than relying on simple Time-Weighted Average Price (TWAP) or Volume-Weighted Average Price (VWAP) execution models, modern bank algorithms use Reinforcement Learning (RL) to execute orders.

For example, J.P. Morgan's DNA (Deep Neural Network for Algo Execution) system utilizes deep neural networks to evaluate tick-by-tick order book queues and spread thickness. The reinforcement learning agent learns the optimal timing to split large parent orders into smaller child clips, minimizing market impact and slippage. Additionally, banks use advanced Natural Language Processing (NLP) models to scan news feeds and central bank statements in milliseconds. These systems generate immediate hawkish/dovish sentiment scores that drive data-trading algorithms, capturing value during the pre-FOMC announcement drift described in academic finance research.

Dynamic Delta-Hedging and the Mechanics of the V-Shape Reversal

One of the most powerful institutional phenomena is the V-shape short squeeze or rotation to the north. This is rarely caused by retail traders buying. Instead, it is the mathematical outcome of options desks re-hedging their books.

When a hedge fund buys a large volume of EUR Call options (bullish EUR) from a bank options desk, the bank is short the call, giving them a negative Delta. To insulate themselves from spot price increases, the bank's automated systems must buy spot EURUSD to remain delta-neutral. Because the bank is short the options, they are 'Short Gamma', meaning their negative delta increases as the spot price rises. If a central bank release surprises dovish, spot EURUSD surges, forcing the bank's option algorithms to buy more spot EURUSD to maintain neutrality. This dynamic creates an automated feedback loop: spot rises, options delta rises, algorithms buy spot, spot rises further. This is the mechanical reality behind vertical short squeezes.

Inventory Management and the 'Hot Potato' Risk Control

When a bank trader buys EURUSD from a client, the bank holds an unbalanced long inventory. To manage this risk, the trader must immediately lay off the position through internal crossing (matching with a buying client) or by selling the EURUSD on wholesale interbank venues like EBS or Reuters Matching.

If the market begins moving against the bank's inventory, their internal pricing engine skews spreads. They will lower bids to disincentivize more sellers and lower asks to attract buyers. Under high-volatility events, banks manage their Value at Risk (VaR) by widening spreads significantly, shifting the risk premium to external market participants and preventing toxic flow from running over their books.

Correlating Your Retail System with Bank Architecture

As retail quant traders, we cannot directly see every bank's internal franchise log or options book. However, we can track the observable consequences of their actions. This is why the TradersAnalytica platform integrates Auction Market Theory (AMT) and cumulative delta tracking.

Our system maps Value Areas, POCs, and Value Migration to define where market-making algorithms are likely to seek balance. By tracking Cumulative Delta, we identify hidden absorption walls where price stops falling despite high seller pressure—the classic signature of bank limit orders absorbing client flows. Furthermore, our Decision Supervisor mimics the banks' internal risk gating. If the ML-projected expectancy of a trade falls below the 45% threshold (such as during the high-volatility FOMC announcement), the system gates execution. This matches the exact capital preservation protocols used by professional quantitative funds.

Use the platform as a decision process.

The goal is not to copy one level. The goal is to learn how auction value, retail behavior, liquidity pressure, delta, and risk rules combine into a trade idea.