The EURUSD Macro Stack: Fed vs ECB, Bond Yields, COT Positioning, and Auction Value

A practical top-down EURUSD framework for reading the Fed/ECB policy path, bond-yield spreads, COT positioning, and auction-market execution levels.

The hierarchy: macro first, execution last

The purpose of this framework is not to predict every EURUSD candle. It is to understand where the market cycle is likely moving, check whether money is already betting in that direction, then wait for auction and flow confirmation before execution.

The professional sequence is simple: macro data changes policy expectations, policy expectations move bond yields, relative bond yields move currencies, positioning shows who is already involved, and auction-market structure tells us where the trade is worth taking.

For EURUSD, this means the pair should not be read as a standalone chart. It should be read as the live expression of the Fed path versus the ECB path.

- Step 1: identify whether the Fed or ECB is becoming more dovish or hawkish faster.

- Step 2: check whether US yields are moving faster than German/Eurozone yields.

- Step 3: use COT and retail positioning to understand crowded or vulnerable sides.

- Step 4: execute only when value, delta, and liquidity confirm the macro story.

Why bond yields are the real forex engine

The main macro driver of EURUSD is not the headline itself. It is the yield repricing after the headline. If US data makes the market price the Fed more dovishly, US yields can fall and the dollar loses support. If Eurozone data makes the market price the ECB more dovishly, Eurozone yields can fall and the euro loses support.

That is why EURUSD is a relative-rate instrument. The question is not only whether US yields rise or fall. The question is whether US yields rise or fall faster than German and Eurozone yields. The spread is the engine.

US Treasuries are a preferred asset class for institutional money because they are liquid, deep, and widely accepted as collateral. When yields are attractive, global capital can prefer dollars. When expected returns on dollars fall, capital can rotate elsewhere.

- Fed more hawkish than ECB: USD yield advantage improves, EURUSD pressured.

- Fed more dovish faster than ECB: USD yield advantage weakens, EURUSD supported.

- Both sides weakening: EURUSD often becomes rotational instead of trending cleanly.

Macro scenario grid

A clean EURUSD view starts by classifying the data. NFP, unemployment, wages, CPI, PCE, PPI, GDP, ISM, PMI, JOLTS, ADP, and jobless claims all matter because they change what the market thinks the Fed or ECB will do next.

The mistake is treating every weak US print as automatically bullish EURUSD or every soft Eurozone print as automatically bearish EURUSD. A very bad US print can initially create dollar demand if it triggers recession panic. A mildly weak US print can weaken the dollar if it simply reduces hike pressure without causing fear.

The framework therefore asks whether data is strong, unchanged, slightly worse, or materially worse, then maps that into policy expectations rather than reacting to the headline emotionally.

- US strong + inflation hot: Fed stays restrictive, EURUSD bearish pressure.

- US weak + inflation cooling: Fed reprices dovish, EURUSD bullish pressure.

- Eurozone inflation sticky: ECB support for EUR can remain alive.

- Eurozone inflation cooling faster than US: EUR support weakens, rallies can fail.

- Both economies weakening: expect rotation, not a clean directional religion.

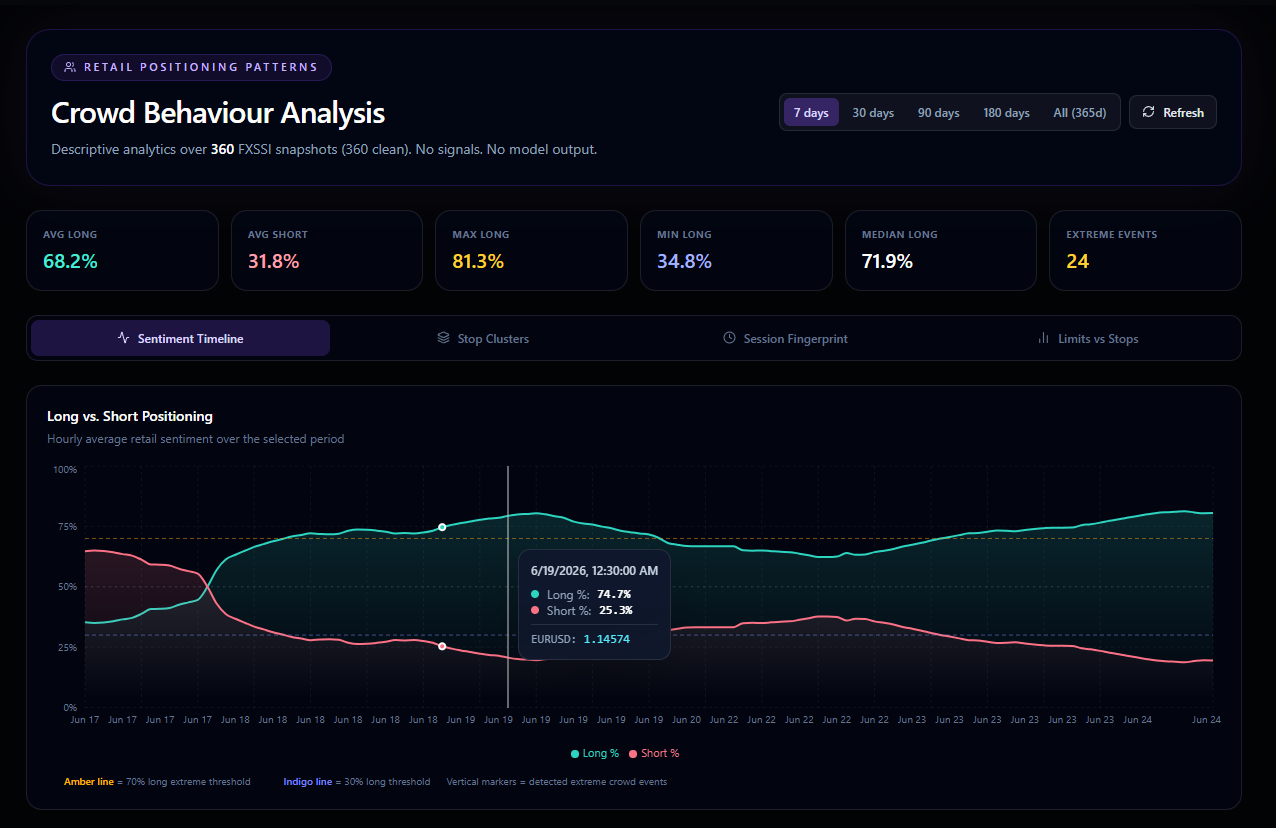

Where COT fits in the stack

The Commitments of Traders report is not an entry signal. It is a weekly positioning map. It tells us how different participant groups are positioned in futures, including non-commercial speculative money and, in the financial futures report, asset managers and leveraged funds.

For EURUSD, COT helps answer two questions: is smart/speculative money already leaning long or short EUR, and is that positioning becoming crowded? If non-commercials are heavily long EUR while price cannot break higher, the upside may be vulnerable. If leveraged funds are short while real money remains long, price can become choppy as short-term sellers fight longer-term allocation flows.

Because COT updates weekly, it belongs above execution but below macro. It helps define the battlefield; it does not tell the trader to click buy or sell.

- Non-commercial positioning shows speculative EUR futures bias.

- Asset-manager positioning can reveal slower institutional allocation.

- Leveraged-fund positioning can reveal fast-money pressure.

- COT is best used with value acceptance, not as a standalone trigger.

Auction market theory turns macro into tradable location

Macro can be right and the trade can still be wrong if the location is poor. Auction market theory solves that problem by asking where the market is accepting value, where it is rejecting price, and whether the day is rotating or migrating.

If EURUSD accepts above prior value, macro bullish pressure has a location to express itself. If EURUSD rejects premium while delta weakens, a bullish macro story may already be priced or temporarily exhausted. If price returns to POC and chops, the market is balancing while waiting for a stronger catalyst.

This is why the system combines macro, COT, value area, POC migration, cumulative delta, and liquidity shelves. A good trade idea needs both a reason and a place.

- Value acceptance confirms that the market is doing business at new prices.

- POC migration shows where the heaviest trade is moving.

- Cumulative delta shows whether aggressive flow agrees with price.

- Retail and stop pools show where forced liquidity may accelerate the next leg.

Current EURUSD operating model

The current EURUSD picture is a policy-transition fight. Weak US labour data damaged the old dollar-bullish story, but softer Eurozone inflation also reduced the euro's own policy support. That means the pair is not cleanly bearish, but it is not confirmed bullish either.

The market is waiting for the next US inflation evidence to decide whether the Fed is truly becoming dovish faster than the ECB. Until that is clear, EURUSD should be treated as a rotational auction unless price proves value migration.

The practical levels are the same levels the system is watching: the 1.1434-1.1437 zone as the value/floor battle, the 1.1458-1.1473 area as premium resistance and trapped-buyer risk, and the 1.1373 area as the lower structural support that would reassert the bearish map if broken.

- Bullish confirmation: hold 1.1434-1.1437, reclaim 1.1452, accept above 1.14728.

- Bearish confirmation: reject 1.1458-1.1473, weaken delta, break and hold below 1.1430.

- Neutral read: chop between 1.1419 and 1.1473 while waiting for CPI and yield-spread confirmation.

Use the platform as a decision process.

The goal is not to copy one level. The goal is to learn how auction value, retail behavior, liquidity pressure, delta, and risk rules combine into a trade idea.